There's a specific kind of dread that comes with opening a credit card bill.

You already know it's bad. You've been avoiding the app for two weeks. But you open it anyway, and the number sitting there — with that minimum payment that barely moves it — just sits on the screen while your stomach drops.

I've been there. I remember feeling like the debt was a permanent fixture of my life. Like it was just something I'd carry forever, paying minimums every month, watching the interest quietly add more back every time I chipped something away. It felt hopeless. And honestly? It felt shameful. Like I had failed at something basic that everyone else seemed to have figured out.

Here's what I need you to hear before anything else: you didn't fail. Credit card debt is one of the most common financial realities in America — and it's designed to be incredibly hard to escape. High APRs, minimum payment traps, and the quiet creep of everyday expenses on a low income make it genuinely difficult. Not impossible. Just difficult.

And difficult problems have solutions. This is yours.

Step 1: Face the Numbers Completely (Even Though It's Terrifying)

You cannot fight something you refuse to look at. This step is emotionally the hardest one — and it needs to happen first.

Sit down with every credit card statement you have. Open every account. Write down the following for each one:

Card name or bank

Current balance

APR (interest rate)

Minimum monthly payment

How long you've had the balance

Put it all on one piece of paper or a simple spreadsheet. Every single card. No hiding.

Why This Matters:

Most people in debt have a vague, anxiety-soaked sense of how much they owe. The actual number — as frightening as it may be — is almost always more manageable to confront than the fog of not knowing. When you can see the full picture clearly, you can make a real plan. The fog is what keeps people stuck.

Take a breath. Write the number down. Then keep reading.

Step 2: Stop the Bleeding Immediately

Before you can pay anything off, you have to stop adding to it. This sounds obvious, but it's the step that actually requires the most honest self-assessment.

The Hard Options (Pick at Least One):

Freeze your cards — literally. Put them in a zip-lock bag, fill it with water, and put it in your freezer. Old trick, but it works. The physical barrier creates just enough friction to stop impulse spending.

Remove saved card numbers from every online store and app. Amazon, DoorDash, Target, everywhere. If buying something requires you to get up and find a card, a huge percentage of impulse purchases just won't happen.

Delete the shopping and delivery apps from your phone entirely for the duration of your payoff journey.

This isn't about punishment. It's about removing the easy paths until you're in a stronger position. You can put the apps back later. Right now, they're costing you money you don't have.

Step 3: The Two Payoff Methods — Choose the One That's Right for You

There are two proven strategies for paying off multiple credit cards. Both work. The right one for you depends on your personality as much as your math.

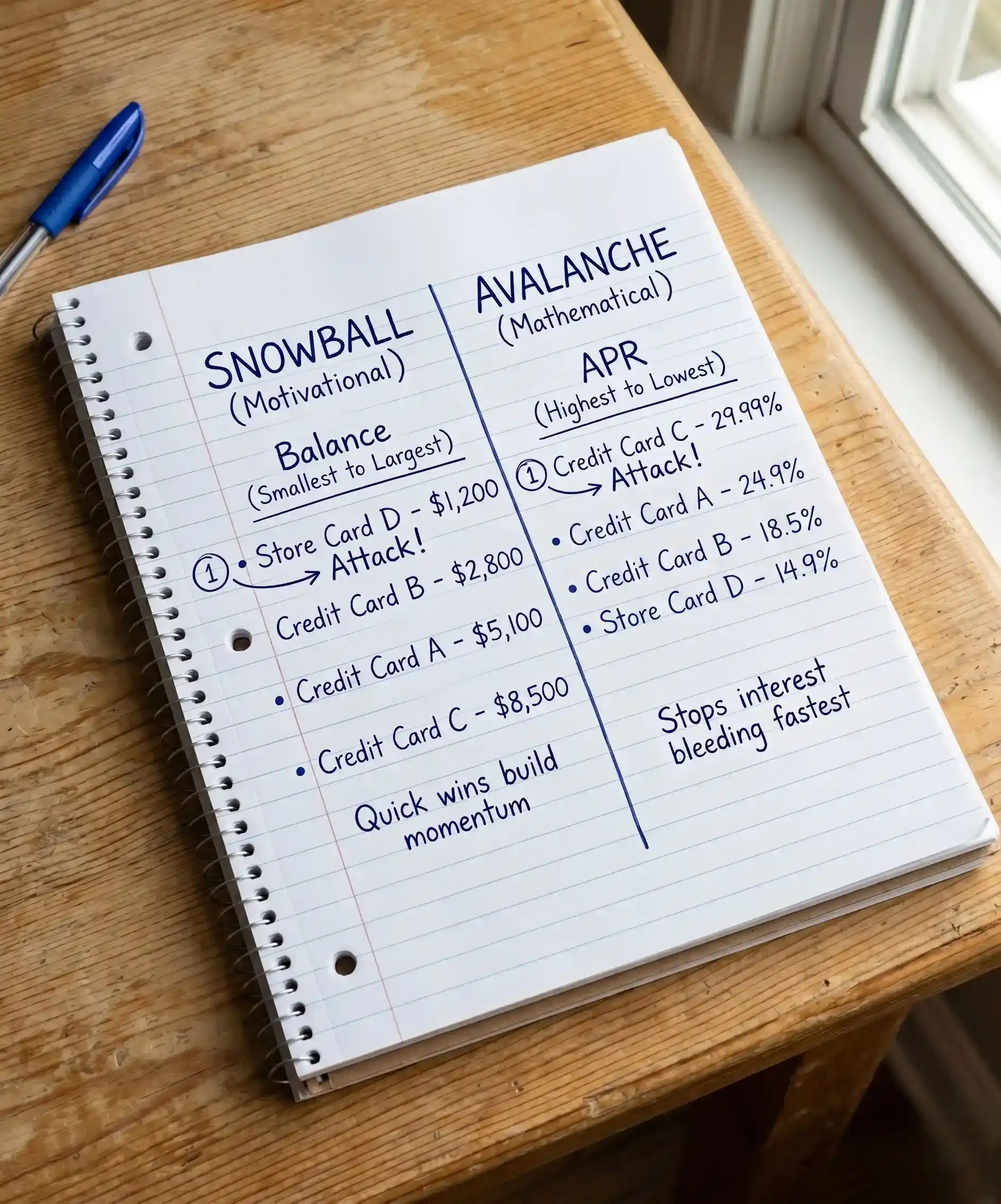

The Debt Snowball Method

How it works: You list your cards from smallest balance to largest, regardless of interest rate. You pay the minimum on everything except the smallest balance — and you throw every extra dollar at that one until it's gone. Then you roll that payment into the next one.

Why it works: The psychological wins of paying off a card completely — even a small one — create real momentum and motivation. Research backs this up. If you've been feeling defeated, the snowball is often the better emotional choice.

The Debt Avalanche Method

How it works: You list your cards from highest APR to lowest. You pay minimums on everything except the highest-interest card — and you attack that one first. Mathematically, this saves more money in interest over time.

Why it works: If you have a card with a 24–29% APR — which is painfully common right now — that interest is actively working against you every single month. Eliminating the highest rate first stops the bleeding fastest in pure financial terms.

My honest recommendation: If you have one card with a dramatically higher interest rate than the others, start there (avalanche). If your rates are similar, go with the snowball and use the motivational wins to fuel your momentum.

Step 4: Call Your Credit Card Company and Ask for a Lower APR

Most people don't know this is possible. It absolutely is — and it takes about 10 minutes.

Credit card companies would rather work with you than lose you as a customer. If you have a decent history with them (even just a year or two of making payments), there is a real chance they'll lower your interest rate if you simply ask. I've done this myself and gotten a rate reduced by 4 percentage points on one card.

A Simple Script You Can Use:

Call the number on the back of your card and say something like this:

"Hi, I've been a customer for [X] years and I've been working hard to pay down my balance. I was hoping to discuss whether there's any possibility of lowering my APR. I'm committed to paying this off, and a lower rate would help me do that faster."

That's it. Be polite, be calm, be direct. They may say no. They may say yes. They may offer a temporary promotional rate. Any of those answers takes two minutes to hear and costs you nothing to ask.

Also Worth Asking About:

Hardship programs — Many major credit card issuers have hardship or financial relief programs that can temporarily reduce your minimum payment or interest rate during a difficult period.

Balance transfer offers — If you receive a 0% APR balance transfer offer, it can be worth exploring, but read the fine print on transfer fees and the terms carefully before acting.

Step 5: Build the Gap — Finding Extra Cash on a Low Income

Here's where the frugal living piece becomes critical. Paying off debt fast requires a gap — money left over after your necessities — and on a low income that gap is small. Your job is to widen it from both sides.

Cut Expenses First (The Faster Side):

Before chasing extra income, squeeze every unnecessary dollar out of your current spending. On a low income, this has the highest immediate impact.

Cook every meal at home — even imperfect, simple meals

Cancel every subscription you don't use actively (audit them tonight)

Switch to a cheaper phone plan (Mint Mobile, Visible, and similar MVNOs offer plans for $15–$30/month)

Drop the grocery store brand loyalty and shop for the cheapest option on every staple

Use the library for books, movies, and free streaming services

Apply for SNAP benefits if you qualify — there is no shame in using programs designed exactly for situations like yours

Generate Extra Income Without Burning Out:

I want to be careful here. I'm not going to tell you to work three jobs or hustle yourself into the ground. Low income often means physically demanding work, and burnout is real. But there are lower-barrier options worth considering:

Sell what you already own. Facebook Marketplace, eBay, Poshmark — a few weekends of honest sorting through your home can generate $100–$400 that goes straight to your balance.

Offer simple services in your neighborhood. Lawn mowing, dog walking, babysitting, cleaning — these require no startup cost and pay in cash.

Mystery shopping and research studies. UserTesting, Survey Junkie, and local university studies pay modest amounts for minimal time commitments.

Seasonal and gig work strategically. One month of part-time seasonal work — tax season, holiday retail, event staffing — and channeling 100% of it to debt can move the needle significantly.

Every extra dollar you find goes to your target card. Every single one. Not to catch up on spending. Directly to debt.

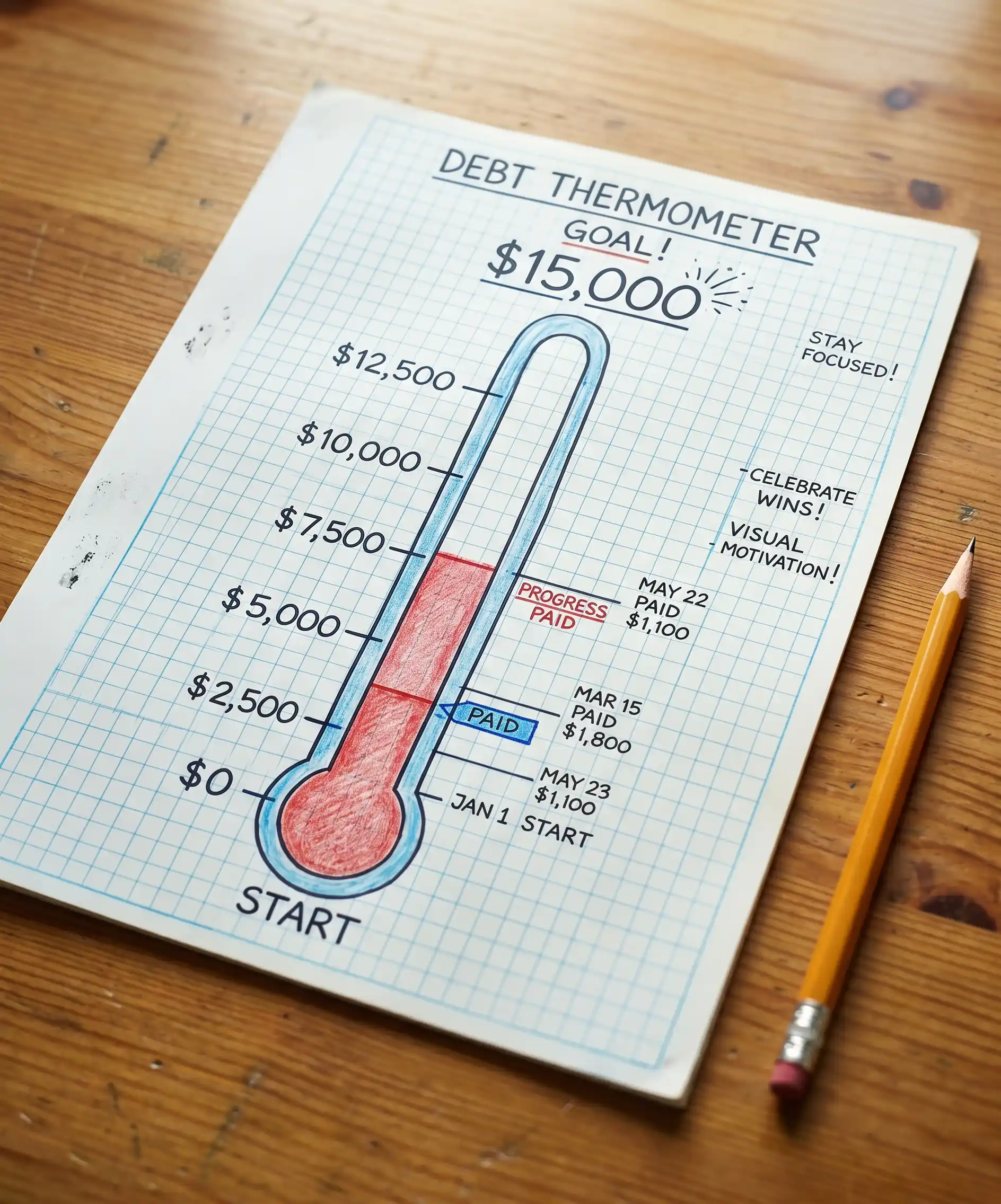

Step 6: Track Every Single Payment and Celebrate Progress

Paying off debt on a low income is slow. I won't lie to you about that. There will be months where unexpected expenses push you back, and it will feel like you're running on a treadmill.

This is exactly why tracking your progress visibly matters so much.

Ways to Track That Actually Work:

The debt payoff thermometer. Draw a simple thermometer on paper, mark your total debt at the top, and color it in as you pay it down. Stick it somewhere you see every day. Visual progress is genuinely motivating.

A simple spreadsheet with each card's balance updated monthly. Watching numbers go down is more powerful than you'd expect.

Celebrate every paid-off card. Not with money. With acknowledgment. Tell someone you trust. Let yourself feel proud. You did something hard.

The Debt Will End. I Promise.

When I was in the middle of paying off debt on a tight budget, someone told me: "The math always works if you stay consistent long enough."

I didn't believe them at the time. I believe them now.

The truth is that credit card debt — even a lot of it — has an end. It is finite. As long as you stop adding to it and make consistent progress, every single month brings you closer to the last payment. That day comes. It really does.

You don't need a high income to pay off debt. You need a clear plan, a method you'll actually stick to, ruthless spending cuts, and the patience to keep going on the months when progress feels invisible. You have all of that in you.

Start tonight. Write down the numbers. Pick a method. Make one call.

Now I'd love to hear from you — what's the biggest challenge you personally face when trying to pay down debt on a tight budget? Is it the interest rate making it feel like you can't get ahead, the irregular income, or just finding extra money to throw at it? Drop it in the comments — your question might help someone else who's reading and feeling exactly the same way.

This post was helpful? Save it to your Pinterest board for when you need a reminder of the plan — and share it with someone you know who's fighting the same battle quietly.

Reader Interactions