Do you ever get to the end of the month and genuinely have no idea where your money went?

Not in a vague way. In a specific, slightly panicked way where you open your banking app, stare at the number, and think — I worked this entire month for that?

That was me about two years ago. I wasn't making bad money. I wasn't carrying massive debt. I just had this constant, invisible leak — coffee here, a Target run there, a random Amazon order that seemed totally reasonable at the time, takeout three times in one week because I was tired. None of it felt like a big decision. All of it added up to a few hundred dollars I couldn't account for every single month.

Then our car needed a repair we hadn't planned for. One $800 bill and my "cushion" was basically gone. I was frustrated, stressed, and — honestly — a little embarrassed. I knew better. I just hadn't been paying attention.

So I did something drastic. I declared a No-Spend Month.

I told my family we were going to spend 30 days cutting every single dollar of discretionary spending we possibly could. No shopping, no eating out, no unnecessary purchases of any kind. Bills paid, basic groceries bought, everything else frozen.

At the end of that month, I had saved just over $500 we would have otherwise drifted through without thinking. And the habits it built? Those lasted way longer than the month did.

Here is exactly how to do it — rules, exceptions, survival tips, and all.

First: What a No-Spend Month Actually Is (And Isn't)

Let's clear this up right away, because the name trips people up.

A No-Spend Month does not mean you pay zero dollars all month. That's not realistic and it's not the goal. You still pay your rent or mortgage. You still pay your utility bills, insurance, subscriptions you genuinely need, and any debt minimums. You still buy groceries — real, actual groceries for real meals.

What you are cutting is every dollar of discretionary spending. That means anything you buy by choice rather than necessity. The coffee run. The new shirt. The weekend trip to HomeGoods. The takeout because cooking felt like too much effort. The app you downloaded on impulse.

The goal is simple: become radically aware of every dollar that leaves your hands this month, and stop every single non-essential one.

That awareness alone is worth more than the money you save.

The Master Rules of the No-Spend Month

These are the ground rules. Post them somewhere you'll see them every day.

Rule 1: Needs Are Allowed. Wants Are Not.

Before you spend any money, ask yourself one question: Is this something I need to live my life this month, or is it something I want? If it's a want — no matter how reasonable it feels — it waits until next month.

Rule 2: No Exceptions That Weren't Pre-Approved

Life will throw surprises at you this month. Some will be genuine emergencies — a medical need, a car repair that affects your ability to get to work, a necessary household fix. Those are allowed. What's not allowed is calling something an "emergency" because you really want it. Be honest with yourself.

Rule 3: Use What You Have

Before this month starts, look at your pantry, your freezer, your closet, and your home. You almost certainly have more than you think. The challenge is to use it up before reaching for your wallet.

Rule 4: The 24-Hour Rule for Temptation

When you feel a strong urge to buy something, write it down and wait 24 hours. Most urges disappear entirely. The ones that don't tell you something about your actual priorities once the month is over.

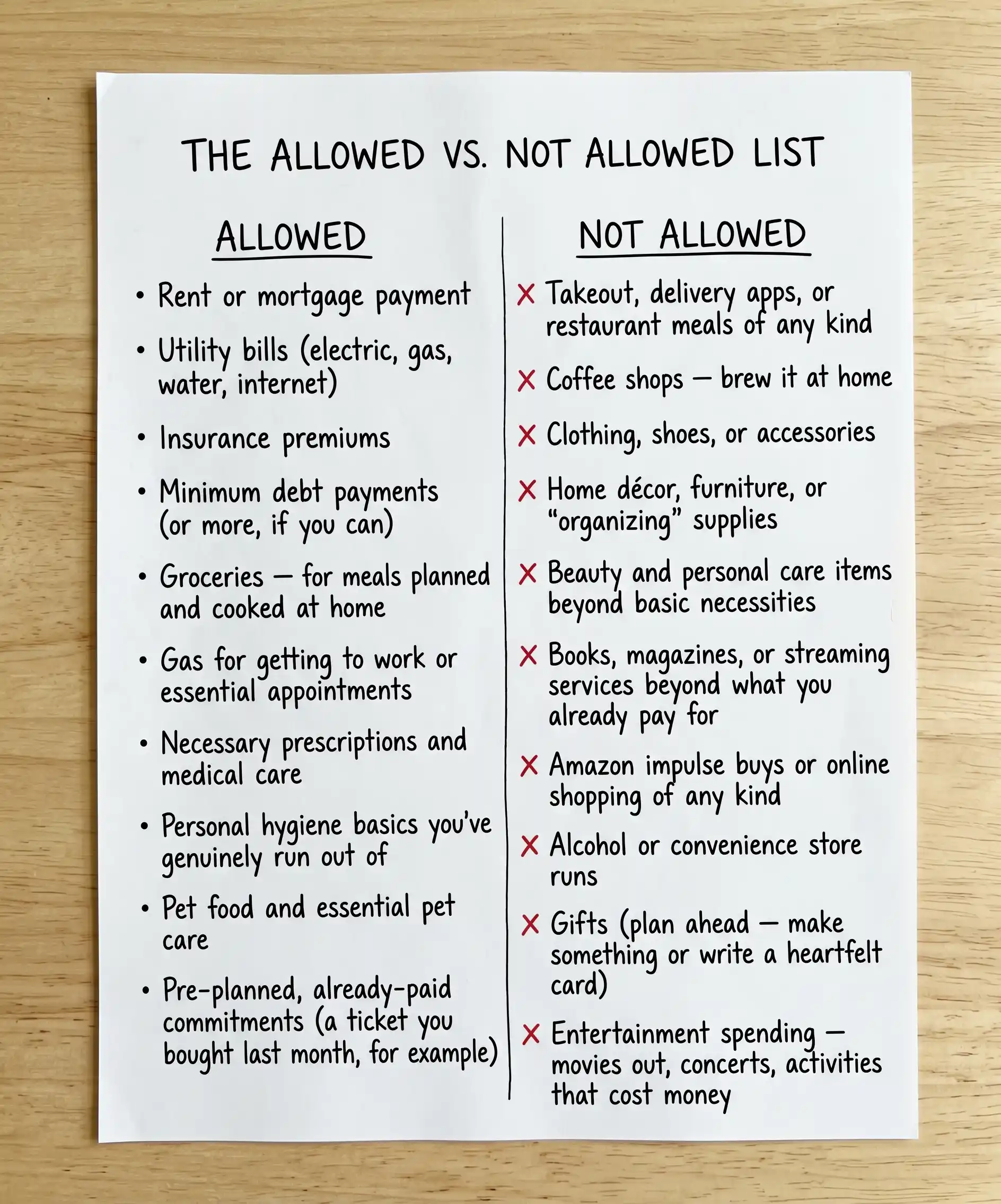

The Allowed vs. Not Allowed List

Print this out. Stick it on your fridge. Refer to it whenever you're not sure.

ALLOWED:

Rent or mortgage payment

Utility bills (electric, gas, water, internet)

Insurance premiums

Minimum debt payments (or more, if you can)

Groceries — for meals planned and cooked at home

Gas for getting to work or essential appointments

Necessary prescriptions and medical care

Personal hygiene basics you've genuinely run out of

Pet food and essential pet care

Pre-planned, already-paid commitments (a ticket you bought last month, for example)

NOT ALLOWED:

Takeout, delivery apps, or restaurant meals of any kind

Coffee shops — brew it at home

Clothing, shoes, or accessories

Home décor, furniture, or "organizing" supplies

Beauty and personal care items beyond basic necessities

Books, magazines, or streaming services beyond what you already pay for

Amazon impulse buys or online shopping of any kind

Alcohol or convenience store runs

Gifts (plan ahead — make something or write a heartfelt card)

Entertainment spending — movies out, concerts, activities that cost money

Your Daily No-Spend Checklist

Every single day this month, run through this list. It takes 60 seconds and keeps you accountable when your motivation starts to wobble.

Morning:

Check your bank balance — know your number

Plan every meal for the day before you leave the house

Make coffee at home before you go anywhere

Write down any spending urges from yesterday — did they pass?

Before Any Purchase:

Is this on the Allowed list?

Is this truly a need or an honest want?

Can I substitute something I already have?

Have I waited 24 hours if this is non-essential?

Evening:

Record every dollar spent today — even allowed spending

Mark today on your tracker (green for no discretionary spending, yellow for a slip, red for a full fail — no shame, just honesty)

Remind yourself of your savings goal before you go to sleep

How to Survive Days 10–14 (The Hardest Part)

Here's what nobody tells you before you start: the first week is surprisingly easy. The novelty carries you. You feel proud and motivated and a little smug.

Then days 10 through 14 hit.

That's when the excitement wears off and the discomfort kicks in. You're bored. You're frustrated. Everything feels like a restriction. You'll convince yourself that one takeout order won't hurt, or that the thing you want to buy is basically a necessity.

This is the wall. Here's how to get through it.

Survival Strategies for the Hard Days:

Fill the time boredom used to fill with spending. Think about it — how many of your purchases happen because you're restless, scrolling, or looking for something to do? Replace that with free activities. A walk. A library book. A free YouTube deep-dive on something you've always wanted to learn. Cook something ambitious you've been putting off.

Call out the feeling, not the craving. When I wanted to order takeout on day 12, it wasn't actually about the food. I was tired. I didn't want to cook. Once I named that, I made a super simple dinner — scrambled eggs and toast — and the feeling passed. The craving is usually a disguise for something else.

Revisit your "why" every single day. Write down your specific savings goal before the month starts and look at it on the hard days. My number was $500 toward rebuilding my emergency fund. That number sitting on a sticky note on my bathroom mirror did more for my motivation than any podcast or app.

Text a friend or your partner on the hard days. Saying out loud "I really want to order pizza tonight but I'm staying on track" is oddly powerful. Accountability that's spoken is stickier than accountability that's just in your head.

Celebrate small wins loudly. Did you make it one week? That's real. Tell someone. Mark it on your tracker. Every no-spend day is money in your pocket — act like it.

How to Set Your $500 Target

Five hundred dollars in one month sounds like a lot. Here's what it actually breaks down to in real life:

Eating out twice a week at ~$15–$20 per outing: ~$120–$160/month

Coffee shop visits 3x a week at ~$6 each: ~$72/month

Random Amazon orders and online impulse purchases: ~$50–$100/month

Convenience store stops, gas station snacks, small purchases: ~$40–$60/month

Target/Walmart "I just needed one thing" runs: ~$60–$100/month

Alcohol, entertainment, or miscellaneous: ~$50–$100/month

Total discretionary drift per month for the average household: $392–$592.

That's not a made-up number. That's exactly where most people's untracked money goes — in small, painless-feeling amounts that add up to something genuinely significant.

The $500 goal isn't aggressive. For most households, it's actually conservative.

What to Do With the Money You Save

The whole point of saving the money is to actually do something with it. Don't let it sit in your checking account where it will slowly disappear again.

The moment the month ends, move the savings immediately:

If you have no emergency fund: Move it there first. Even $500 changes how a financial emergency feels.

If you have high-interest credit card debt: Throw it at the highest-interest balance.

If your basics are covered: Start a dedicated savings goal — a car repair fund, a vacation fund, a future down payment.

The point isn't just the money. It's the proof you can save it.

One Month Changes More Than Your Bank Account

I'll be honest with you — the $500 was great. But the bigger win from my first no-spend month was what it did to my relationship with spending.

After 30 days of pausing before every purchase, I couldn't go back to mindless buying. I'd pick something up in a store and just... put it back down. Not because I told myself I couldn't have it. Because I'd gotten so used to asking "do I actually want this?" that most of the time the honest answer was no.

That habit is priceless. And it all started with one deliberately uncomfortable month.

You can do this. Thirty days. That's it.

Now I want to hear from you — if you were to start your No-Spend Month this week, what do you think your single biggest temptation would be? For me it was takeout on tired weeknights, without question. Drop yours in the comments — and if you've already done a no-spend challenge, I'd love to hear how much you saved!

Save this post to your Pinterest board so you can come back when you're ready to start — and share it with a friend who needs a financial reset this month.

Reader Interactions